401(k) Plan Tax Credit Summary

Eligible employers may be able to claim a tax credit of up to $5,000, for three years, for the ordinary and necessary costs of starting a SEP, SIMPLE IRA or qualified plan (like a 401(k) plan.) A tax credit reduces the amount of taxes you may owe on a dollar-for-dollar basis.

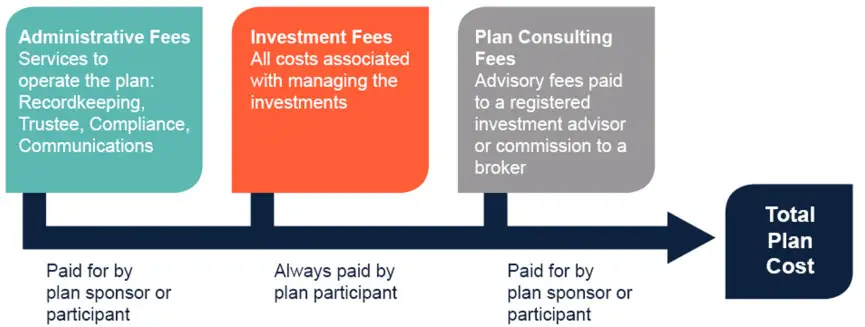

Retirement Plan Fees

Retirement plan fees are complicated. Between administration, investment management, recordkeeping, consulting, revenue sharing, sub-TA and 12b-1, it isn’t always clear to plan participants or plan sponsors exactly what they’re paying, how much they’re paying or even who’s paying the fees.

Keep Your Plan Assets Safe

Cyber fraud is a growing concern globally. Individuals are typically very careful to keep their bank account and email authentication information safe, but they aren’t always smart with the rest of their personal information.

Target Date Funds—Does One Size Really Fit All?

If you have ever opened a brokerage account with an advisor, you know the first step is gathering information to determine the risk profile and appropriate investment allocation for the individual.

QDIA…Why is it important?

The qualified default investment alternative (“QDIA”) is arguably the most important investment in a plan’s investment menu. By far the most often selected QDIA investment is a target date fund (“TDF”). TDFs are typically the only investment selection that offers unitized professionally managed portfolios that reflect the participants’ time horizon today and as they go to and through retirement.

Excessive Fee Litigation: The Best Defense is Compliance

Excessive fee litigation is increasing at a steady pace and all signs are it will continue to increase. The positive side of this situation is that we now have more caselaw to consider as we work toward compliance in creating a “best defense”. Early caselaw did not reflect the consistency of court decisions. Some court rulings were in direct conflict with those of other courts, and some did not seem well reasoned.

Retirement Plan Committee Activities

A retirement plan committee consists of co-fiduciaries who are responsible for all plan management activities that have been delegated to them by their plan’s named fiduciary.

IRS Audit Tips

The Internal Revenue Service’s (IRS’s) Employee Benefit Audit Program is used to audit and enforce. The IRS’s emphasis, with respect to defined contribution plans is on compliance with the requirements of the Internal Revenue Code (the Code), the plan’s tax qualification and administration of all plan documents. In the event of noncompliance with regulations, the IRS can impose taxes, penalties and interest.

Collective Investment Trusts

For almost a century, collective investment trusts (CITs) have played an important role in the markets. They were originally introduced in 1927.

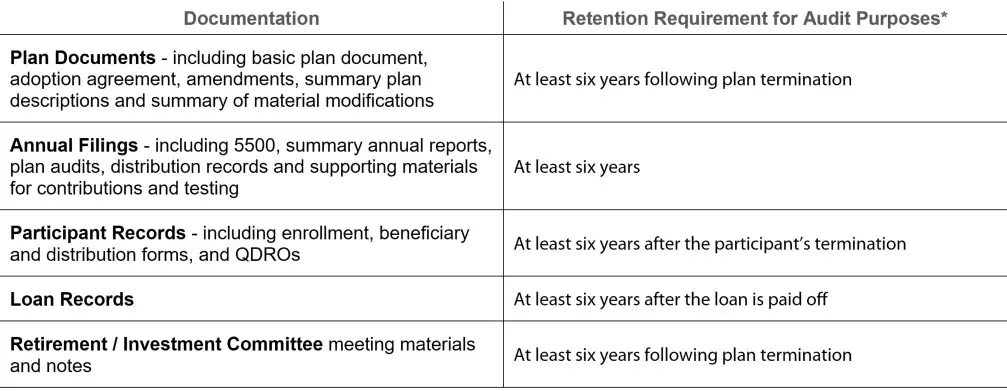

Record Retention

You don’t need to be a magician to know what records to keep and for how long. While most providers can supply reports and plan documents, the plan administrator remains ultimately responsible for retaining adequate records that support the plan document reports and filings. Refer to the chart below to know which documents you need to keep in case of a plan audit.